Minnesota Senator Jeremy Miller also recently introduced the Minnesota Bitcoin Act, allowing state investments in Bitcoin and exempting crypto gains from state income tax. On the federal level, Representative Ro Khanna is confident that Congress will pass stablecoin and crypto market regulation this year, though he voiced concerns over President Trump’s involvement with his meme coin.

North Dakota Tightens Crypto ATM Regulations

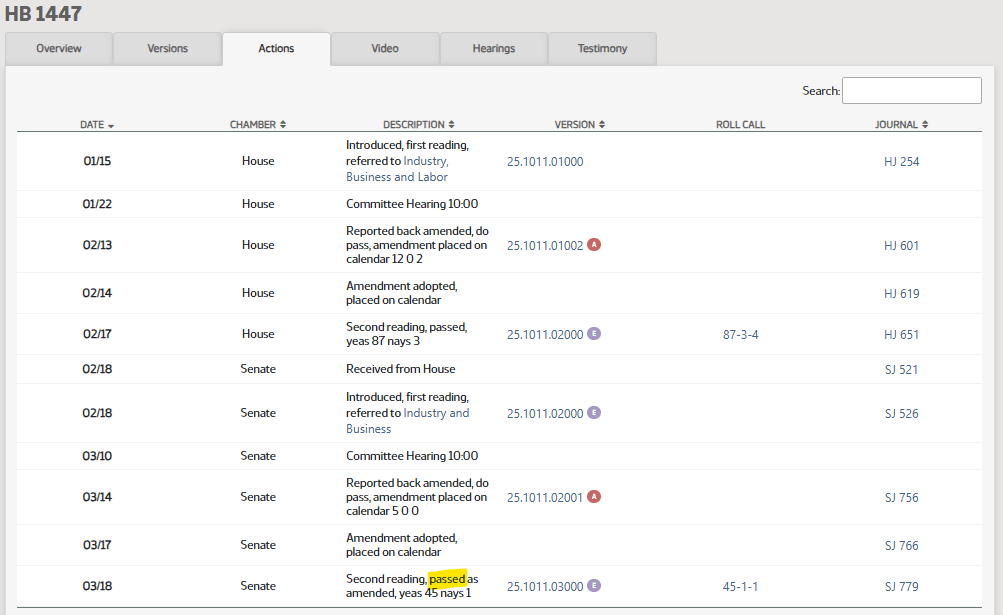

The North Dakota Senate passed House Bill 1447 in a decisive 45-to-1 vote, reintroducing a provision that limits daily crypto ATM transactions to $2,000 per user. The bill was originally introduced on Jan. 15, and its main goal is to protect residents from scams by establishing new regulatory requirements for crypto ATMs and their operators.

Initially, the bill proposed a $1,000 daily transaction cap, but the state’s House later adjusted the limit to $2,000 per day for the first five transactions in a 30-day period. The Senate now reinstated a firm $2,000 cap without the five-transaction clause. The legislation must return to the House for approval before reaching Governor Kelly Armstrong, who will decide whether to sign it into law.

Under the bill’s provisions, crypto ATM and kiosk operators will be required to get a state money transmitter license, enforce the $2,000 daily transaction limit across their entire ATM network, and display fraud warnings at machines. Additionally, operators have to employ blockchain analytics to detect suspicious transactions and report any fraudulent activity to authorities. They will also be obligated to submit quarterly reports with details about their kiosk locations, operator identities, and transaction data.

Representative Steve Swiontek, the bill’s primary sponsor, believes there is a serious need for regulation, and stated that the absence of adequate safeguards allowed criminals to exploit crypto ATMs for fraudulent schemes. The initiative passed after a similar law passed in Nebraska on March 13, known as the Controllable Electronic Record Fraud Prevention Act. At the federal level, US Senator Dick Durbin of Illinois also introduced comparable legislation on Feb. 25, because of a case in which a constituent was tricked into depositing $15,000 into a crypto ATM under the false pretense of avoiding arrest.

According to the Federal Trade Commission, fraud losses linked to Bitcoin ATMs surged almost tenfold between 2020 and 2023, and exceeded $65 million in the first half of 2024 alone. Consumers aged 60 and older were found to be three times more likely to fall victim to such scams.

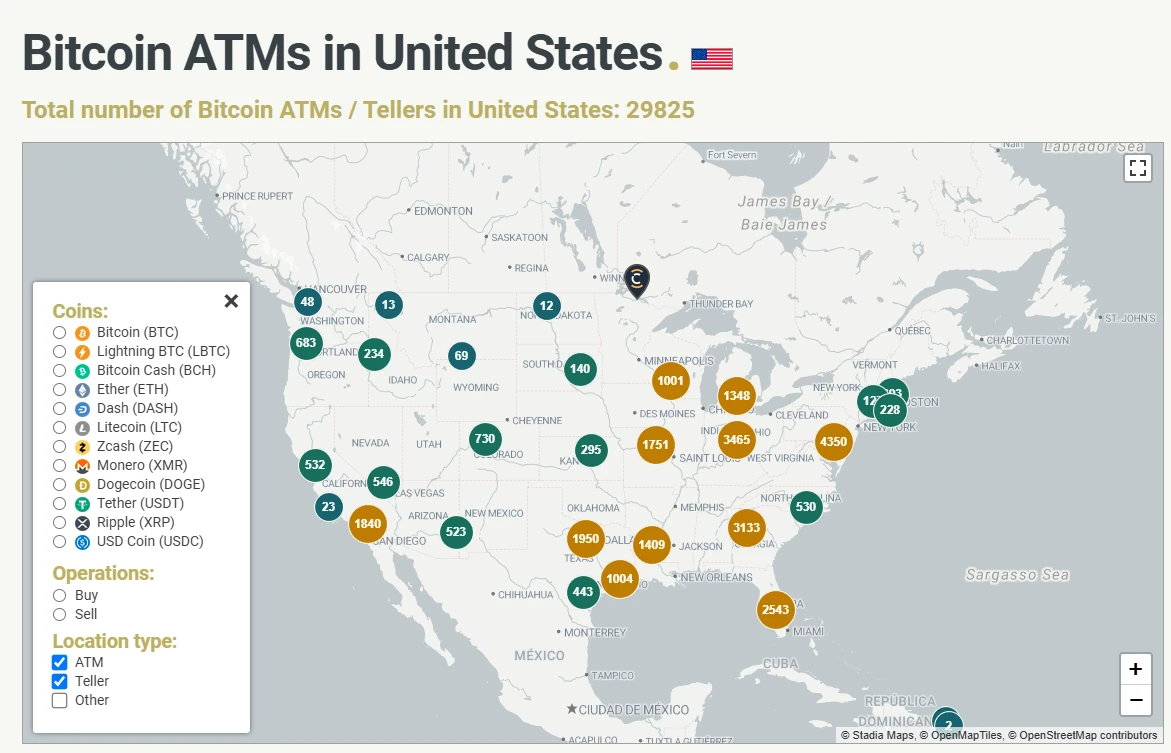

(Source: Crypto ATM Radar)

Despite the risks, the United States continues to lead the global crypto ATM market, and hosts 29,822 machines, which account for 78% of the total worldwide. Canada follows with 3,486 machines, while Australia ranks third with 1,613 crypto ATMs.

Minnesota Senator Proposes Bitcoin Investment Bill

Other US states are also making moves in the crypto space. Minnesota state Senator Jeremy Miller introduced the Minnesota Bitcoin Act, which is a huge shift in his stance on Bitcoin.

Miller was initially very skeptical, but explained that after conducting extensive research and hearing from constituents, he became convinced of Bitcoin’s potential and broader cryptocurrency adoption. The proposed bill aims to increase financial opportunities for Minnesotans by allowing the Minnesota State Board of Investment to invest state assets in Bitcoin and other digital currencies.

The legislation will also enable Minnesota state employees to add Bitcoin and other cryptocurrencies to their retirement accounts. Additionally, residents will have the option to pay state taxes and fees using Bitcoin, following the lead of states like Colorado and Utah, which already accept cryptocurrency for tax payments. Louisiana also embraced digital currencies for state services.

One of the bill’s most noticeable provisions is the exemption of investment gains from Bitcoin and other cryptocurrencies from state income taxes. Under current US tax law, taxpayers can deduct up to $10,000 in state tax payments from federal taxes, but any amount beyond that remains taxable at both state and federal levels.

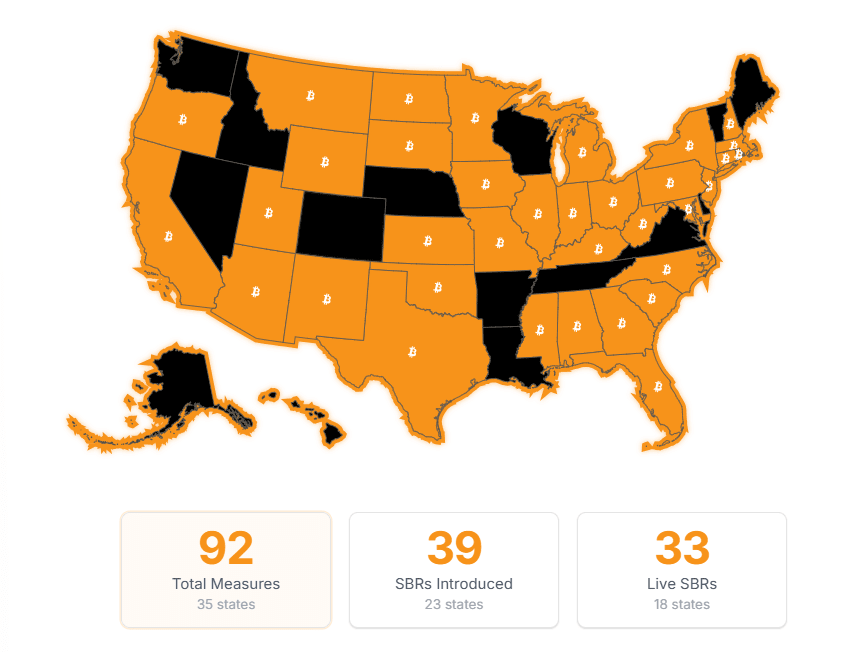

States considering Bitcoin reserves (Source: Bitcoin Laws)

Minnesota is now among a growing number of US states introducing Bitcoin reserve bills. According to Bitcoin Laws, 23 states proposed similar legislation to establish Bitcoin reserves. The movement is part of a broader national push, including Senator Cynthia Lummis’ Strategic Bitcoin Reserve Act, which was introduced last July. This federal proposal calls for the US government to accumulate 200,000 Bitcoin annually over five years, ultimately amassing a reserve of one million Bitcoin. More recently, Lummis reintroduced the BITCOIN Act on March 12, which could allow the government to hold an even larger reserve of digital assets.

Bitcoin’s increasing adoption by governments and institutions reflects its impressive long-term performance. Between August 2011 and January 2025, Bitcoin recorded a compound annual growth rate of 102.36%, which is much higher than the S&P 500’s 14.83% return.

US Lawmaker Confident Crypto Regulation Will Pass

Meanwhile, US Representative Ro Khanna of California is confident that Congress could pass both a stablecoin bill and a broader crypto market structure bill this year. He pointed out that there is growing support among Democrats, and even stated that 70 to 80 members now recognize the importance of stablecoin legislation in expanding US influence by increasing global access to dollars.

Stablecoins have become a crucial financial tool, particularly in developing countries where access to physical dollars is limited. Several stablecoin bills are currently under consideration in Congress, including the GENIUS Act in the Senate.

Ro Khanna at the Digital Assets Summit

Khanna also pointed to the Financial Innovation and Technology for the 21st Century Act, known as FIT21, which he co-authored with former Representative Patrick McHenry, as a potential framework for regulating the crypto market. While he acknowledged that some adjustments may be needed, he is optimistic that a foundational market structure bill will take shape.

Many industry executives believe that clear regulatory guidance for digital assets will have a more positive impact on the sector than the recently signed executive order establishing a strategic Bitcoin reserve. In fact, many cryptocurrency prices, including Bitcoin, have declined since the order was issued.

Despite his strong advocacy for blockchain and cryptocurrency regulation, Khanna is still very concerned about President Donald Trump’s involvement in the space through the Official Trump meme coin. He argued that elected officials should not be associated with these kinds of projects, as they detract from the core technological advancements in blockchain. He also warned that these distractions make it harder to convince the public of the legitimate value of the underlying technology.

The controversy surrounding Trump’s meme coin raised many ethical and national security concerns. California Representative Maxine Waters suggested that the token could open the door to corruption, while Representative Sam Liccardo introduced legislation to ban US presidents, members of Congress, senior government officials, and their families from issuing or endorsing cryptocurrencies, securities, or commodities.