Circle Internet Financial is taking significant steps to deepen its role in the traditional financial system, filing an application for a national bank license just weeks after its high-profile IPO. At the same time, JPMorgan analysts have begun coverage of Circle’s stock with an underweight rating and a notably lower price target, highlighting concerns over valuation, competition, and evolving regulatory requirements in the stablecoin sector.

Circle Applies for National Bank License Following Blockbuster IPO

Circle Internet Group (NASDAQ: CRCL), the company behind the $61.5 billion USDC stablecoin, has officially applied for a national banking license, according to a report from Reuters. The application represents a bold new phase in the fintech firm's effort to cement its role within the traditional financial system — just weeks after its red-hot initial public offering sent shockwaves through both Wall Street and the crypto world.

If approved, the license from the US Office of the Comptroller of the Currency (OCC) would authorize Circle to operate a national bank under the name First National Digital Currency Bank, N.A. The institution would not, however, function as a full-service bank. It would not be permitted to take cash deposits or make loans like traditional lenders. Instead, its role would be more specialized: acting as a custodian for Circle's reserves and offering digital asset custody services to institutional clients.

Circle's ambition to obtain a US bank charter dates back several years, with previous reports speculating on various routes — from an industrial bank license to a national trust charter. The company consistently denied those particular intentions, but its latest application to the OCC makes clear that Circle is ready to take a more regulated and centralized position in the financial ecosystem.

The OCC has not yet publicly confirmed receipt of the application, nor provided a timeline for a decision. However, if granted, Circle would become one of the first major crypto-native companies to receive a national bank charter.

IPO Euphoria and Institutional Confidence

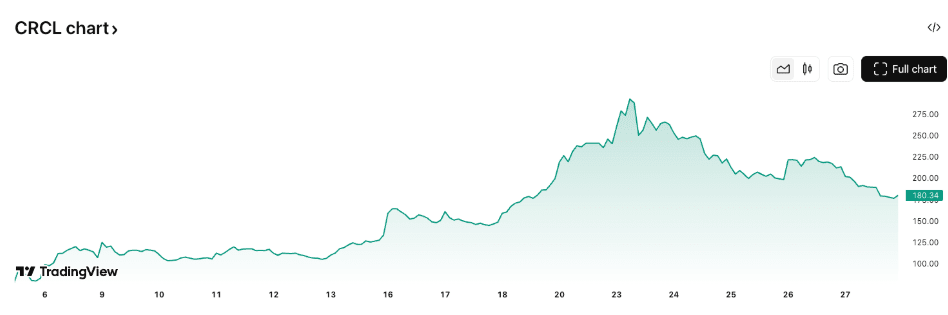

Circle’s bid comes on the heels of a historic public debut. Listed under the ticker CRCL on June 5, the company's IPO was 25 times oversubscribed, pricing above the indicated range at $31 per share. The stock then soared 167% on its first day of trading, closing at $82.80. As of Monday, CRCL closed at $181.29, putting its market capitalization above $40 billion — more than double its valuation just a few weeks ago.

Circle (CRCL) shares tumbled 15.5% Friday (Source: TradingView)

The IPO performance was widely interpreted as a signal that institutional investors are hungry for regulated, transparent exposure to the digital asset economy. With the GENIUS Act — recently passed by the US Senate — laying the groundwork for comprehensive stablecoin regulation, Circle is well-positioned to benefit.

Analysts at Bernstein said this week that USDC is likely to emerge as the “largest regulated stablecoin” under the GENIUS Act, granting Circle a substantial first-mover advantage over rivals like Tether and PayPal USD.

Founded in 2013, Circle has evolved from a digital payments startup to one of the most pivotal players in the blockchain ecosystem. Its USDC stablecoin is fully backed by dollar-denominated assets and is widely used for cross-border payments, decentralized finance (DeFi), and tokenized financial instruments.

While other stablecoins such as Tether’s USDT have faced criticism over transparency, Circle has actively leaned into regulatory compliance. The company publishes monthly attestation reports and is known for maintaining one-to-one reserves in cash and short-term Treasuries.

A national banking license could further enable Circle to manage those reserves internally, reducing reliance on third-party custodians and potentially streamlining compliance obligations under US law.

Moreover, by creating a dedicated federally chartered bank for digital currencies, Circle could also pave the way for other crypto companies to follow suit — a potential game-changer for the institutional adoption of blockchain technology.

A Pivotal Moment for Crypto and Banking

Circle’s application comes at a time when the lines between traditional finance and digital assets are blurring. Tokenized Treasury bills, crypto-collateralized loans, and stablecoin payments for real-world goods are becoming more common. And regulators, once wary of crypto’s decentralized ethos, are now working to integrate compliant actors into the legacy system.

If the OCC grants the license, it would signal a major shift in US banking policy toward embracing blockchain infrastructure, particularly at the federal level.

JPMorgan Initiates Coverage of Circle with Underweight Rating and $80 Price Target by 2026

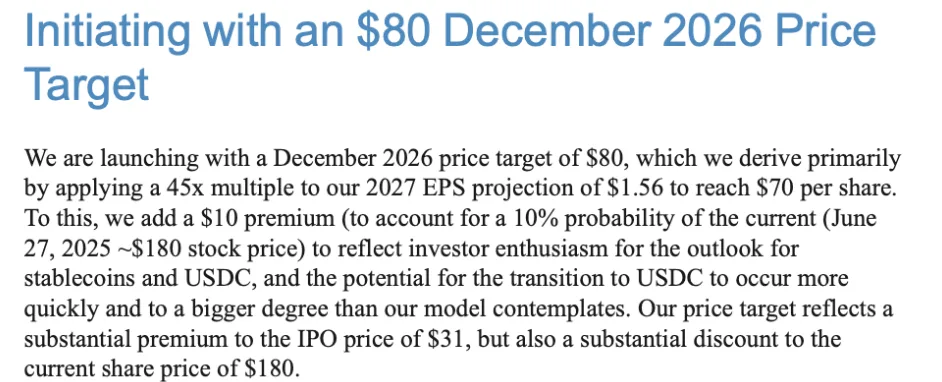

In related news, JPMorgan Chase, one of the largest and most influential US investment banks, has officially initiated analyst coverage of Circle Internet Financial (NASDAQ: CRCL) with an “underweight” rating and a 12-month price target of $80 by December 2026. The coverage marks the first major Wall Street evaluation of the recently public stablecoin issuer — and it comes with a stern warning about valuation risks and competitive pressures in the digital asset ecosystem.

The forecast, shared Monday in JPMorgan’s North America Equity Research report led by senior analyst Kenneth Worthington, projects a 55% decline from Circle’s current share price of around $180. The investment bank’s $80 target is based on a 45x multiple of the company’s projected 2027 earnings per share (EPS), with an added $10 premium to account for potential upside.

An excerpt from JPMorgan’s North America Equity Research (Source: JPMorgan)

While JPMorgan acknowledges Circle’s growing role in the blockchain-powered financial infrastructure and its early mover advantage in the stablecoin sector, the note casts doubt on the company’s ability to sustain its current market valuation in the face of mounting headwinds.

JPMorgan also believes the stock has overheated in the post-IPO euphoria, especially given that the company’s core business — stablecoin issuance — remains relatively nascent and untested at scale in fully regulated environments.

“Our Dec-2026 price target of $80 implies a market cap of approximately $21 billion,” the report said, suggesting that the market has overestimated Circle’s near-term profitability and long-term defensibility.

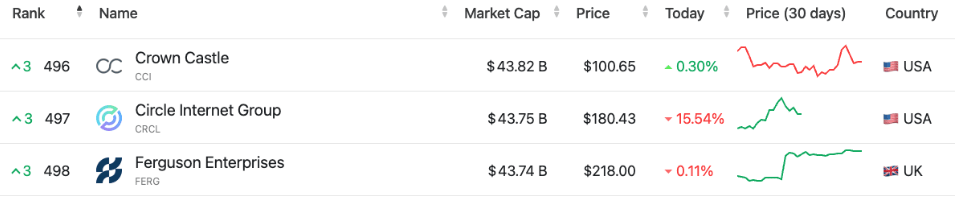

Circle is the 497th largest company worldwide (Source: CompaniesMarketCap)

Competitive Threats and Low Switching Costs

A key concern for JPMorgan is the evolving competitive landscape within crypto payments and digital asset custody. Although Circle’s USD Coin (USDC) is one of the most widely used and regulated stablecoins globally — with a market cap of $61.5 billion — the analysts argue that Circle’s dominance may be more fragile than it appears.

“We see competition as a potential threat to Circle,” the note stated, pointing to the rise of tokenized deposit accounts, digital money market funds, and rival stablecoins.

Because many of Circle’s business models operate in a low-switching-cost environment, JPMorgan warns that new entrants could erode its market share by replicating Circle’s infrastructure and leveraging the very networks Circle helped build.

JPMorgan’s report also highlights regulatory risks as a significant overhang for Circle’s long-term valuation. The analysts noted that upcoming stablecoin legislation in the United States — including potential capital reserve requirements similar to Europe’s MiCA framework — could constrain Circle’s ability to grow USDC issuance.

While the firm appears well-capitalized to handle current obligations, new laws might compel Circle to allocate more equity against its stablecoin liabilities, reducing flexibility and dampening returns.

Another major concern comes from central bank digital currencies (CBDCs), particularly in foreign markets. Though the US has so far leaned into private-sector stablecoins as a way to preserve dollar hegemony, other countries may opt for government-backed digital currencies that bypass private issuers like Circle altogether.