In This Article

If there's a future money, CBDCs might be that future! Full meaning being Central Bank Digital Currencies, CBDCs present a new way for governments to issue and manage money. Unlike decentralized cryptocurrencies, CBDCs are controlled by central banks. These digital currencies are designed to be stable and secure, offering a government-backed alternative to traditional electronic payments.

The widespread interest in CBDCs stems from their potential to streamline financial systems. A recent experiment by Sandbox further explores more CBDC use cases across simulated digital trade, tokenized assets, and FX networks. By reducing the need for physical cash, they could make transactions faster and safer.

Governments and central banks see CBDCs as a way to enhance financial inclusion and improve the efficiency of monetary policy. Many countries worldwide are exploring CBDCs, reflecting a global shift towards digital finance. Nations look to central bank digital currencies to provide a reliable and state-backed option amidst the rising popularity of cryptocurrencies and stablecoins.

Central banks play a crucial role in this transformation, aiming to keep up with technological advancements while maintaining control over monetary systems.

The Concept of Central Bank Digital Currencies (CBDCs)

Central Bank Digital Currencies (CBDCs) represent a new form of currency issued digitally by a nation's central bank. They are designed to function like physical cash but in a digital format.

Definition and Overview

CBDCs are a digital form of a government's fiat currency. Unlike cryptocurrencies like Bitcoin, which are decentralized, CBDCs are centralized and issued by the central bank. This means the government backs them, and they can be used as legal tender, like physical money.

CBDCs aim to provide a secure and efficient way of transferring money. They can reduce the costs associated with physical cash, improve financial inclusion by providing access to banking services, and enhance the efficiency of the payment system.

Additionally, CBDCs offer the advantage of being traceable, which can help reduce illegal activities and improve the implementation of monetary policies. Mykola Demchuk, Lawyer & Head of Compliance Consulting at AMLBot, had the following to say:

“One of the reasons why CBDC could be a solution is that CBDC transactions could be tracked using blockchain… The other reason is that CBDC transactions in some instances can be intercepted by a central bank, be stopped and/or funds be confiscated. Therefore all these features will make it very unattractive for criminals to use CBDC for money laundering.”

Types of CBDCs

There are two main types of CBDCs: wholesale CBDCs and retail CBDCs.

Wholesale CBDCs are designed for financial institutions and are used for large-scale transactions. These can help reduce the time and cost of transactions between banks and other financial entities, often utilizing blockchain technology to ensure security and efficiency.

Retail CBDCs are intended for the general public. They allow individuals to hold and spend digital money directly without a bank account. Retail CBDCs can be accessed through digital wallets on smartphones or other devices, making everyday transactions easier and more secure.

The Evolution of Money and Digital Currency

Money has transformed significantly from its earliest forms to modern digital currencies. This evolution highlights the increased efficiency and security in transaction methods.

Historical Overview

Money started as items like shells, stones, and metals for trading goods. These items had intrinsic value or widespread acceptance.

Gradually, societies shifted to metal coins because they were durable and universally accepted. Coins were later replaced by paper money, which was cheaper to produce and transport.

Bank notes emerged as a reliable means of exchange backed by reserves such as gold. The 20th century saw a move towards electronic money, enabling seamless payments and transactions across distances.

From Physical to Digital: A Transformation

The rise of technology introduced digital currencies. Initially, it was electronic money used in bank transfers and online transactions.

Central Bank Digital Currencies (CBDCs) emerged as digital forms of fiat money. Central banks manage these and rely on blockchain technology for security and efficiency.

Unlike traditional electronic money, CBDCs provide more direct access to the central bank's funds, reducing transaction risks and enhancing the payment system's efficiency.

CBDCs are being explored globally to address traditional banking issues and leverage the benefits of digital transactions. For more on this, check out the Atlantic Council's work.

Technology Behind CBDCs

Central bank digital currencies (CBDCs) rely on advanced technology to ensure efficiency, security, and trustworthiness. Key aspects include the use of blockchain and strong security protocols.

Blockchain and Distributed Ledger Technology

Most CBDCs leverage blockchain or distributed ledger technology (DLT). These technologies allow for decentralized recording of transactions, ensuring transparency and reducing the risk of fraud. Each transaction is recorded in a block and linked to the previous ones in a secure chain.

This linked chain makes altering transaction records extremely difficult, enhancing security. DLT also allows multiple nodes to have synchronized versions of the ledger, promoting resilience against outages or single points of failure. The decentralization inherent in blockchain systems is crucial for the consistent and reliable operation of CBDCs.

By using blockchain, central banks aim to offer a digital currency that is both secure and efficient. This technology also facilitates real-time transactions and settlements, significantly reducing costs and the time required for processing payments compared to traditional banking systems.

Security Features and Protocols

Security is of paramount importance for CBDCs. Central banks implement robust encryption techniques to protect digital currency from cyber attacks. Each transaction is secured using cryptographic algorithms, ensuring only authorized parties can access and verify data.

CBDCs also incorporate multi-factor authentication and biometric verification to strengthen user authentication processes. These security measures help prevent unauthorized access and reduce identity theft risk.

Another critical aspect involves the use of consensus mechanisms within blockchain networks. These mechanisms, such as Proof of Work (PoW) or Proof of Stake (PoS), ensure that multiple parties verify and approve all transactions, diminishing the possibility of tampering or fraud.

Through these protocols, CBDCs aim to maintain integrity and trust, ensuring that the digital assets remain secure and reliable for users. Central banks continuously update and refine these security measures to adapt to emerging threats and technological advancements.

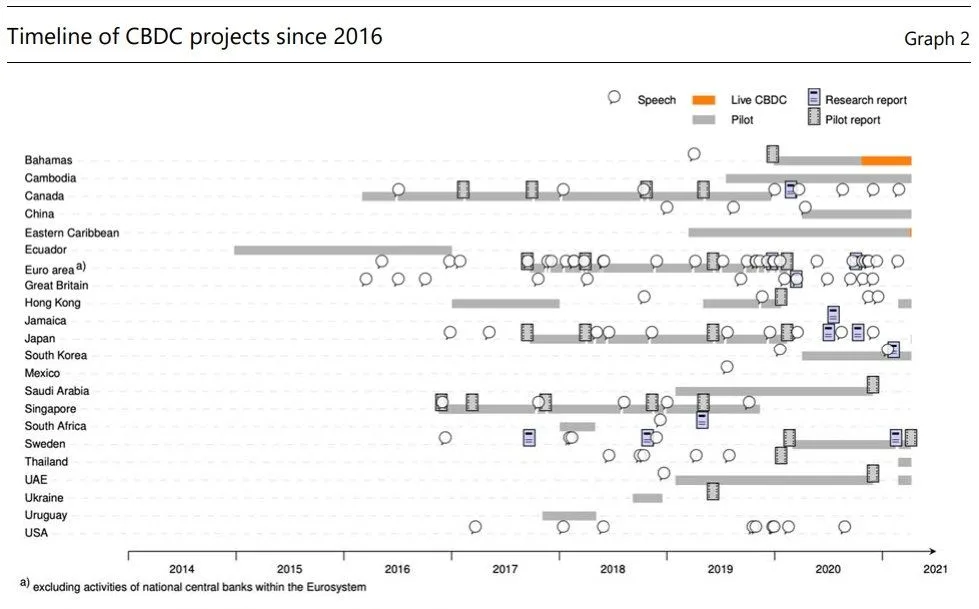

Global CBDC Initiatives

Many countries are progressing in developing Central Bank Digital Currencies (CBDCs), showcasing various stages and approaches. These efforts highlight real-world case studies and pilot projects that bring insights into the potential benefits and challenges of CBDCs.

Pioneering Countries in CBDC Development

Several countries are at the forefront of CBDC development. China has led the pack with its Digital Yuan, which is already used in several cities and for various transactions. But not without criticisms, as American investor and entrepreneur Balaji Srinivasan commented:

"I don’t want to see a digital yuan world. To have every transaction centrally tracked in that way by a hostile state is like slapping a digital dog collar on your neck."

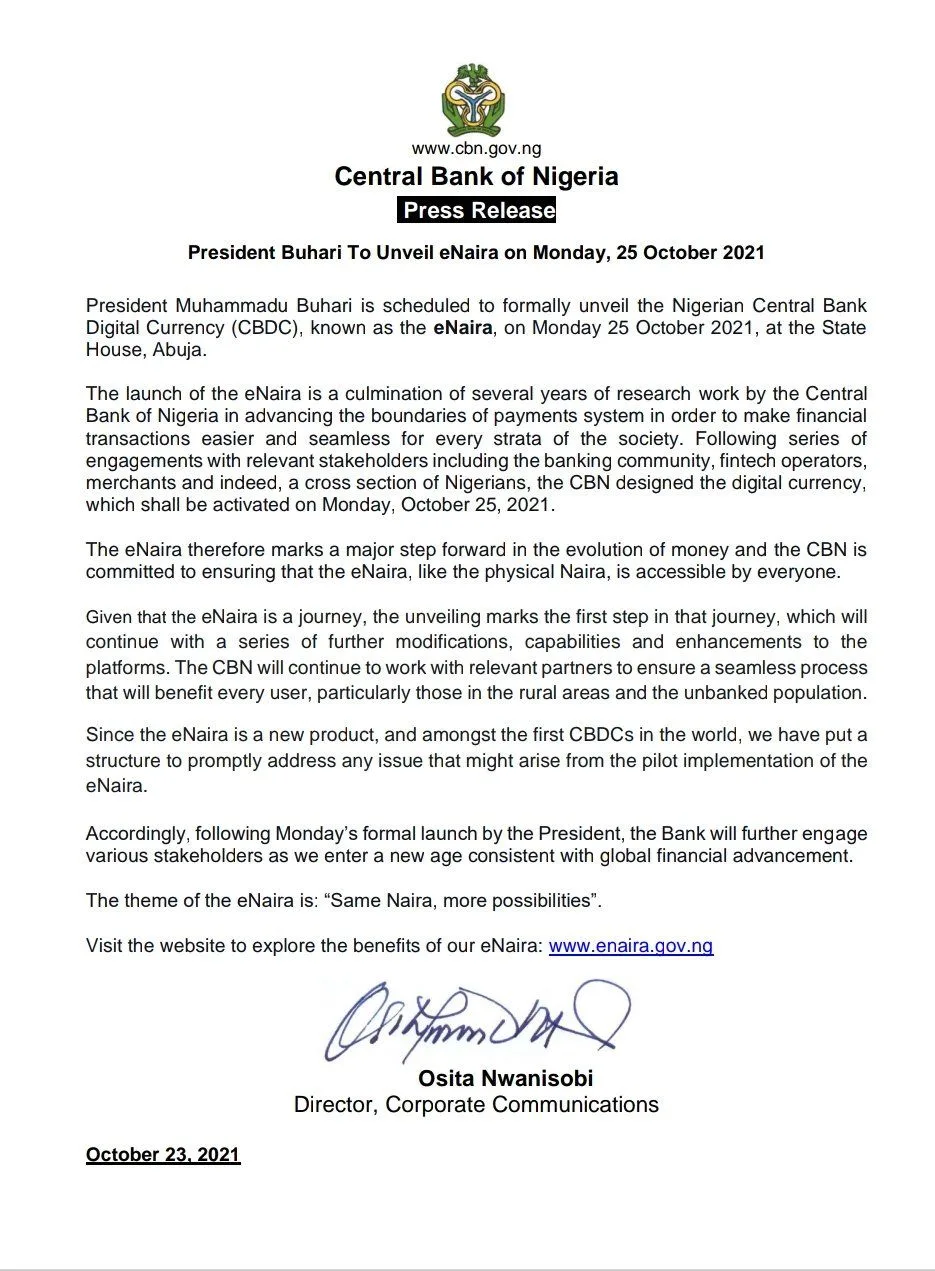

Aside from the Digital Yuan, the European Central Bank is considering a digital euro, targeting a possible release within the next few years. The Bahamas launched the Sand Dollar to improve financial inclusion across its islands. Sweden is testing the e-krona to move towards a cashless society. Nigeria introduced the eNaira to enhance its digital payment system.

Case Studies and Pilots

China's digital yuan pilot has been one of the most extensive, involving millions of users and transactions ranging from retail purchases to governmental payments. This project has provided valuable insights into large-scale implementation and user adoption.

The Bahamas' Sand Dollar aimed to provide efficient financial services to remote areas, offering a successful model for similar regions. Sweden's e-krona experiment has focused on ensuring that the digital currency can work seamlessly across different platforms and services.

Nigeria's eNaira rollout includes both commercial banks and fintech firms, demonstrating a collaborative approach to digital financial innovation. These examples illustrate diverse strategies and highlight critical aspects of CBDC deployment.

Economic Impact

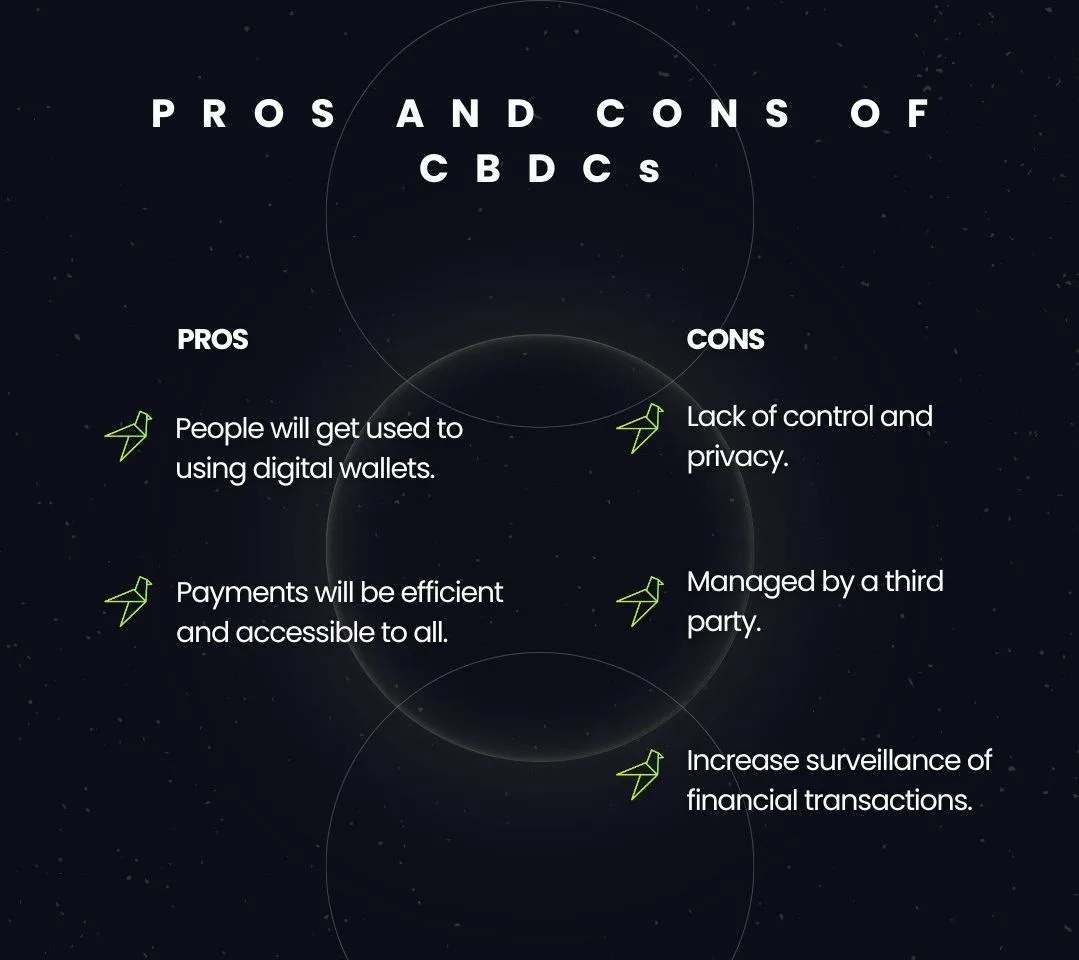

The deployment of CBDCs can significantly impact various economic elements. They provide a more efficient payment system, reducing transaction costs and speeding up transactions. This efficiency can lead to increased economic activity.

CBDCs can promote financial inclusion by providing unbanked populations access to digital financial services. With easy access and low costs, more people can participate in the economy.

Accessibility is key. However, stakeholders must consider potential risks, such as cybersecurity threats and technological failures. These issues need to be addressed to ensure the smooth implementation of CBDCs.

Monetary Policy Considerations

CBDCs can influence monetary policy by providing central banks with precise tools to manage the economy. They can also directly control the money supply and more effectively implement interest rates.

For example, central banks can create a central bank digital currency that is interest-bearing, influencing how consumers spend or save money. An example is the heavily criticized expiration date feature attached to the Digital Yuan. This capability enhances the central bank's ability to stabilize the economy during financial crises.

The introduction of CBDCs might also reduce the reliance on traditional banking systems. This shift could alter liquidity provision and loan distribution, which needs careful monitoring and adjustment.

Legal and Regulatory Framework

Establishing a robust legal and regulatory framework is essential for the successful rollout of CBDCs. This framework must address the balance between privacy and preventing illicit activities.

Regulations must define the role of central and commercial banks in issuing and managing CBDCs. Clear guidelines on data protection, transaction monitoring, and user identification are important.

Additionally, legal challenges like defining digital currency in law, jurisdictional issues in cross-border transactions, and users' digital identities must be carefully evaluated. Creating comprehensive laws will facilitate the secure and efficient implementation of CBDCs.

Challenges in Implementing CBDCs

Implementing Central Bank Digital Currencies (CBDCs) involves several challenges. These include addressing technical issues, ensuring privacy and security, and achieving cross-border interoperability.

Technical Challenges

CBDCs rely heavily on advanced technologies like distributed ledger technology (DLT). This technology requires significant infrastructure upgrades.

Building this infrastructure is costly and time-consuming. Central banks need to ensure seamless integration with existing financial systems. This includes systems used by banks, businesses, and consumers.

Scalability is another critical issue. The system must handle a large volume of transactions without delays. Achieving this requires high-performance computing and robust network capabilities.

Lastly, the system must be resilient to technical failures, including data loss, hardware malfunctions, and cyberattacks. Ensuring this level of reliability is a major technical challenge.

Privacy and Security Concerns

Privacy is a critical issue for CBDCs. Users need assurance that their transaction data is secure. Central banks must find a balance between privacy and law enforcement needs. Many see CBDCs as a potent weapon against money laundering. However, other prominent figures like former US President Donald Trump and Florida Governor Ron DeSantis do not appreciate the privacy and control concerns associated with CBDCs.

Certain user data might need to be accessible to track and prevent illicit activities. However, as certain anti-CBDC ads also suggest, this raises concerns about surveillance and data misuse.

Security is also paramount. CBDCs are digital and, therefore, vulnerable to hacking. Protecting against cyber threats requires advanced encryption and other security measures.

Implementing these security measures is complex and requires continuous updates to counter evolving threats.

Cross-Border Interoperability

Cross-border transactions present additional hurdles. CBDCs from different countries need to interact seamlessly, and this requires setting international standards for interoperability.

Currency conversion is another challenge. CBDCs must facilitate easy and fair currency exchanges. This requires advanced algorithms and cooperative agreements between central banks.

Legal and regulatory frameworks vary globally. Achieving harmonization is difficult but essential. This involves tackling differences in financial regulations and standards among countries.

The Future of Money

Central bank digital currencies (CBDCs) aim to transform how money is used, stored, and managed. They promise increased efficiency and security in financial systems.

Innovations and Trends in Digital Currencies

Digital currencies are evolving rapidly. Blockchain technology is driving many innovations, offering secure, transparent transactions. Several countries are exploring or implementing CBDCs. For example, China has already begun trials with its digital yuan, showcasing its potential for faster, more seamless transactions.

CBDCs could reduce costs associated with printing physical money. They also provide better tracking and control of money flow, helping to combat illegal activities. Additionally, digital currencies can facilitate international trade by eliminating currency conversion hassles.

Moreover, digital wallets linked to CBDCs could increase financial inclusion, especially for people without access to traditional banking. This makes money management more accessible to many underserved populations globally.

The Role of CBDCs in Future Economies

CBDCs could significantly impact future economies by providing a stable, government-backed alternative to private cryptocurrencies. They offer the potential for more secure and efficient monetary policies, and central banks can use CBDCs to control the money supply and inflation better.

CBDCs can also improve the efficiency of payment systems. Transactions can be processed faster with lower fees compared to traditional banking. They allow financial systems to be more resilient to crises by reducing reliance on private banks.

Economic stability could benefit, too, as CBDCs reduce risks associated with bank runs by ensuring direct access to central bank money. Additionally, they could enhance transparency and trust in the financial system, fostering a more stable economic environment.