In This Article

Investors looking for stable income and portfolio diversification often turn to bonds, one of the oldest and most widely used financial instruments. However, Bond ETFs (Exchange-Traded Funds) have become an increasingly popular way to access the bond market.

While both investments are designed to provide exposure to fixed-income securities, they work in very different ways. Buying an individual bond means lending money directly to a government or corporation, while a bond ETF allows investors to gain exposure to a diversified basket of bonds through a single tradable fund.

Understanding the differences between bond ETFs and individual bonds is essential for building an effective investment strategy. This guide explains how each investment works, their advantages and disadvantages, and which type of investor they may be best suited for.

What Are Bonds?

A bond is a debt security issued by governments, municipalities, or corporations to raise capital. When you purchase a bond, you are essentially lending money to the issuer in exchange for periodic interest payments and the return of your principal at maturity.

Typical features of bonds include:

Face value (par value): The amount returned to the investor at maturity

Coupon rate: The interest rate paid on the bond

Maturity date: The date when the principal is repaid

Issuer: Government, corporation, or municipality

Bondholders typically receive regular interest payments and their principal when the bond matures, assuming the issuer does not default.

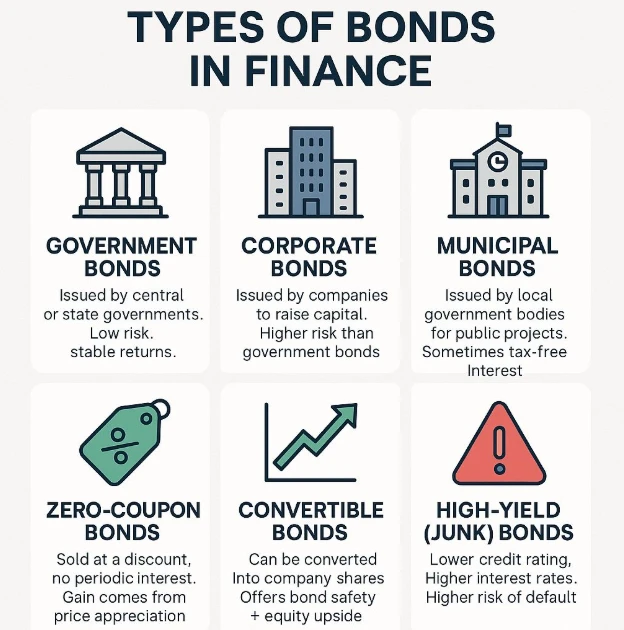

Types of Bonds

Investors can choose from several bond categories, including:

Government bonds: Issued by national governments and considered low risk

Municipal bonds: Issued by local governments and often offer tax advantages

Corporate bonds: Issued by companies, typically offering higher yields but more risk

Treasury bonds: Long-term government bonds with maturities up to 30 years

Because bonds usually pay predictable income and return principal at maturity, they are often considered lower-risk investments compared with stocks.

What Is a Bond ETF?

A Bond ETF is an investment fund that holds a collection of bonds and trades on a stock exchange like a stock. Instead of buying one bond, investors purchase shares of the ETF, which represent ownership in a diversified portfolio of bonds.

Most bond ETFs are index-tracking funds, meaning they aim to replicate the performance of a bond index such as government bonds, corporate bonds, or global bond markets.

Key characteristics of bond ETFs include:

Diversification: Exposure to many bonds in one investment

Stock-like trading: Shares can be bought and sold throughout the trading day

Lower entry cost: Investors can purchase even a single ETF share

Transparency: ETF holdings and prices are visible in real time

Because they hold large baskets of securities, bond ETFs make it easier for investors to gain broad exposure to fixed-income markets without selecting individual bonds themselves.

How Bond ETFs and Bonds Work Differently

Although both investments are tied to bonds, their structure and behavior differ in several important ways.

Ownership Structure

When you buy an individual bond, you directly own that specific debt instrument. This means you receive interest payments and your principal when the bond matures.

In contrast, when you buy a bond ETF, you own shares of a fund that holds many bonds. You do not own the individual bonds themselves, but you benefit from the performance of the overall portfolio.

Maturity

Individual bonds have a fixed maturity date, meaning investors know exactly when they will receive their principal back.

Bond ETFs typically do not mature because the fund constantly buys and sells bonds to maintain its investment strategy or index composition.

Liquidity

Bond ETFs can be traded throughout the day on stock exchanges, similar to stocks. Individual bonds, however, may not trade frequently, and liquidity can vary depending on the issuer and market conditions.

Diversification

Buying a single bond exposes an investor to the risk of that issuer alone. A bond ETF spreads risk across many bonds, issuers, and maturities, which helps reduce the impact of any single default or credit event.

Advantages of Individual Bonds

Individual bonds offer several benefits that appeal to certain investors.

Predictable Income

Bonds typically pay fixed interest at regular intervals, allowing investors to know exactly how much income they will receive.

Return of Principal at Maturity

If the issuer remains solvent, investors receive their original investment back when the bond matures.

Greater Control

Investors can select bonds with specific:

Maturity dates

Credit ratings

Issuers

Interest rates

This allows them to tailor investments to their financial goals.

Reduced Market Price Risk if Held to Maturity

Even if bond prices fluctuate during the holding period, investors who hold bonds until maturity typically receive their full principal.

Advantages of Bond ETFs

Bond ETFs have grown rapidly because they simplify access to the bond market.

Instant Diversification

A single bond ETF can provide exposure to hundreds or thousands of bonds, reducing issuer-specific risk.

Lower Investment Requirements

Buying individual bonds often requires large capital commitments, while bond ETFs allow investors to start with smaller amounts.

High Liquidity

Bond ETFs trade on exchanges and can be bought or sold anytime during market hours.

Lower Costs

Many bond ETFs have relatively low expense ratios compared with actively managed funds and other investment products.

Simplicity

Investors do not need to analyze or select individual bonds; the ETF handles portfolio construction automatically.

Risks of Bonds and Bond ETFs

Both investment types carry risks, including:

Interest Rate

Risk When interest rates rise, bond prices typically fall.

Credit Risk

Issuers may default on payments, particularly with lower-quality corporate bonds.

Market Risk

Bond ETF prices fluctuate with the market because they trade like stocks.

However, diversification in bond ETFs can help reduce some credit risk compared with holding a single bond.

When to Choose Bonds vs Bond ETFs

Bonds may be better for investors who:

Want predictable income and principal repayment

Prefer holding investments until maturity

Want control over individual securities

Bond ETFs may be better for investors who:

Want diversification with a single investment

Prefer flexibility and liquidity

Have smaller investment amounts

Want easy access to broad bond markets

In practice, many investors combine both bonds and bond ETFs to balance control, diversification, and liquidity.

Bond ETFs vs Bonds: Key Differences

| FEATURE | BOND ETFS | INDIVIDUAL BONDS |

| Structure | Fund holding many bonds | Direct ownership of a single bond |

| Diversification | High diversification across many bonds | Limited unless many bonds are purchased |

| Trading | Trades throughout the day like a stock | Often traded through brokers, less liquid |

| Maturity | No fixed maturity | Fixed maturity date |

| Investment size | Low minimum investment | Often requires larger capital |

| Income | Income distributed from fund holdings | Fixed interest payments |

| Control | Limited control over underlying bonds | Full control over bond selection |

| Risk | Diversified risk across many issuers | Exposure to individual issuer risk |

Final Thoughts

Both bond ETFs and individual bonds play important roles in fixed-income investing. Bonds offer predictable income and principal repayment, while bond ETFs provide diversification, liquidity, and easier access to the broader bond market.

For many investors, the best approach is not choosing one over the other, but combining them within a diversified portfolio. By understanding how each investment works, investors can better align their fixed-income strategy with their financial goals, risk tolerance, and investment timeline.