In This Article

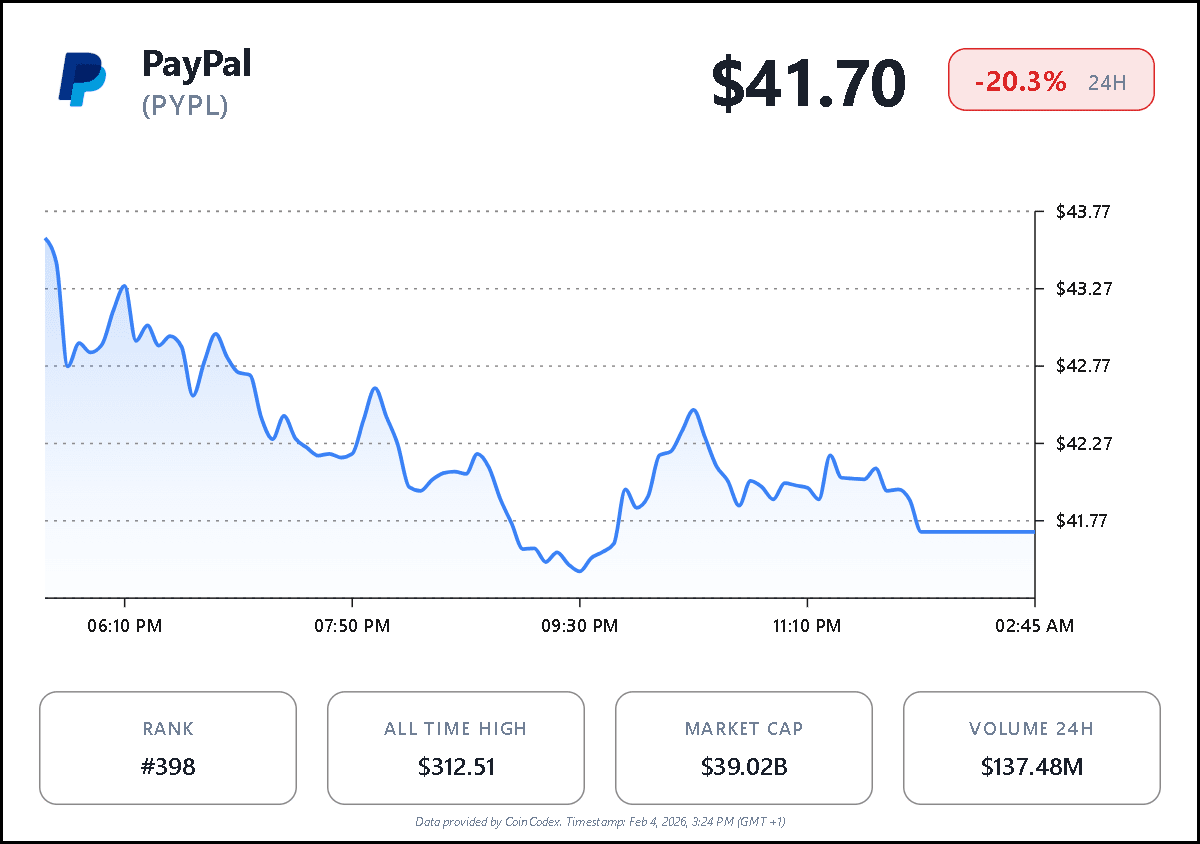

PayPal Holdings Inc. shares traded sharply lower as of the latest session, closing at $41.70, down 20.31% in a single day. The selloff followed the company’s fourth-quarter 2025 earnings release, which revealed weaker-than-expected results. Investors reacted swiftly as earnings and revenue fell short of Wall Street estimates.

The decline marked one of the steepest single-day drops for PYPL in recent years and pushed the stock toward a key technical support zone near the $42 level. Would buyers step in at these levels, or would selling pressure persist?

Earnings Miss Triggers Investor Concerns

PayPal reported non-GAAP earnings per share of $1.23 for the fourth quarter of 2025, missing the Zacks Consensus Estimate of $1.29. The figure still reflected a 3.4% year-over-year increase, yet markets focused on the miss. Net revenues reached $8.68 billion, representing a 3.7% increase on a reported basis and 3% on a forex-neutral basis.

However, the revenue figure came in below expectations of $8.77 billion. The results highlighted a gap between growth momentum and market forecasts, which pressured the stock.

Payment Volume Grows as Engagement Slips

Total payment volume reached $475.14 billion in the quarter, rising 8.5% year over year on a reported basis. On a currency-neutral basis, TPV increased 6%. Transaction revenues climbed 3% to $7.82 billion, while value-added services revenue jumped 10.2% to $857 million. Despite these gains, engagement metrics softened.

Payment transactions per active account fell 4.8% year over year to 57.7, signaling slower usage intensity. That trend raised questions about PayPal’s ability to drive sustained transaction growth.

User Growth and Regional Performance

PayPal ended the quarter with 439 million total active accounts, reflecting 1.2% year-over-year growth. The platform processed 6.75 billion payment transactions, up 2% from the prior year. In the United States, net revenues rose 4.5% to $4.94 billion, accounting for 57% of total revenue.

International revenues reached $3.73 billion, growing 2.7% on a reported basis and 1% on a currency-neutral basis. Slower international growth reflected macroeconomic pressures and competitive dynamics in key markets.

Margins, Expenses, and Cash Position

Operating expenses totaled $7.17 billion in the quarter, increasing 3.5% year over year. The transaction expense rate improved slightly to 0.89% from 0.91% a year earlier. Transaction margin narrowed by 50 basis points to 46.5%, reflecting cost pressures and pricing dynamics.

PayPal closed the quarter with $14.8 billion in cash, cash equivalents, and investments. Operating cash flow reached $2.4 billion, while adjusted free cash flow totaled $2.1 billion. The company returned $1.5 billion to shareholders through share repurchases during the quarter.

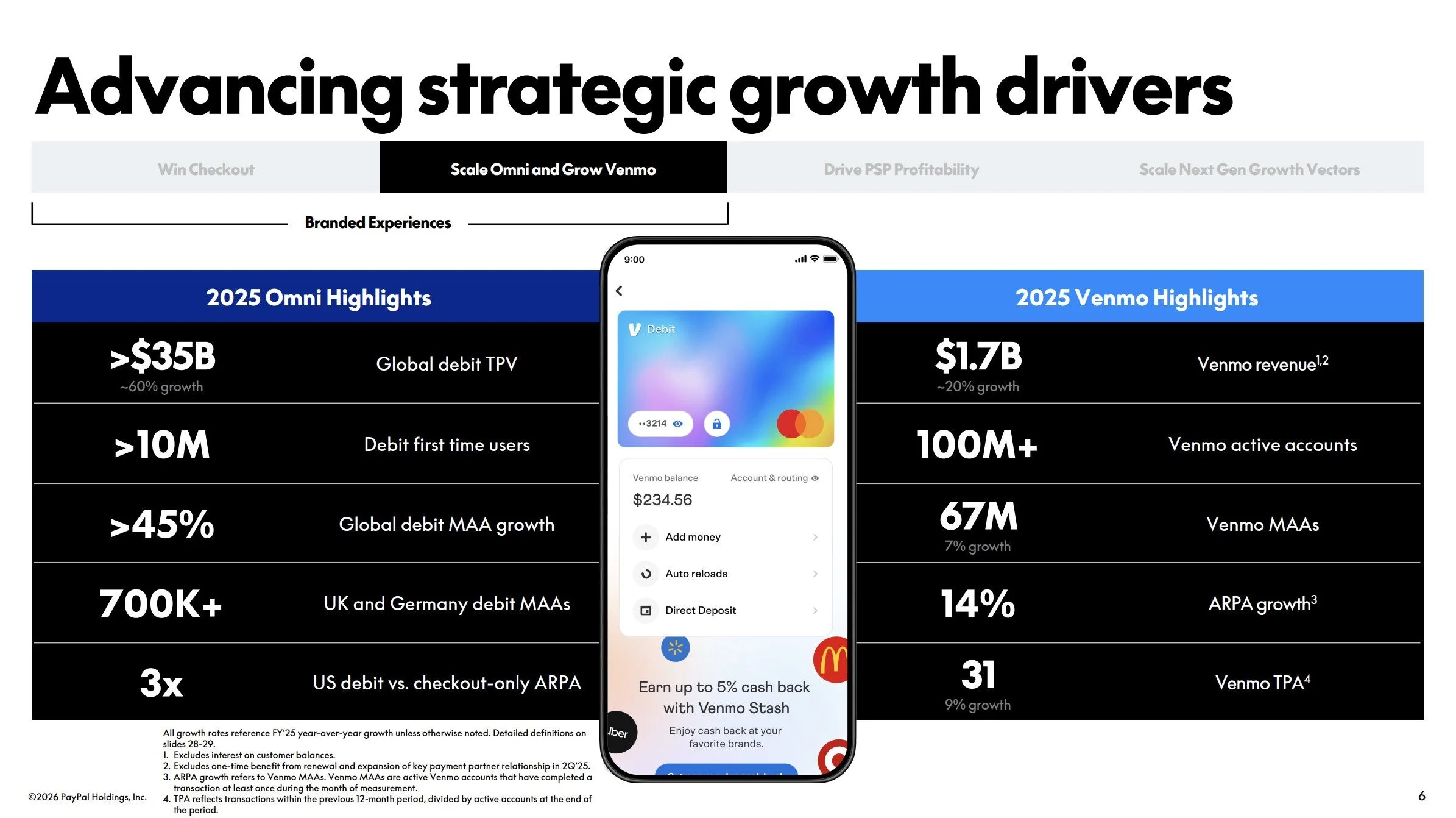

Venmo Strength and Business Highlights

Venmo delivered strong performance, with revenue rising about 20% to $1.7 billion in 2025. Venmo TPV increased 13% in the fourth quarter, while monthly active accounts rose 7% year over year. Enterprise payments recorded seven consecutive quarters of profitable growth and returned to double-digit volume growth.

Source: PayPal Holdings Inc. via X

Buy now, pay later volume surpassed $40 billion for the year, reflecting more than 20% annual growth. These segments showed resilience even as core checkout activity slowed.

Outlook and Forward Guidance

For 2026, PayPal expects non-GAAP EPS to range from a low-single-digit decline to slightly positive growth. Management projects a slight decline in transaction margin dollars and anticipates non-transaction operating expenses to grow about 3%. Adjusted free cash flow should exceed $6 billion, with planned share repurchases of roughly $6 billion.

For the first quarter of 2026, PayPal expects non-GAAP EPS to decline in the mid-single digits. The outlook reinforced investor caution and shaped the sharp market reaction.