Global liquidity indicators moved higher again, but Bitcoin still failed to react in a clear way. Two charts shared on X tracked rising global M2 trends and a late 2025 jump in U.S. repo liquidity, while BTC stayed near the top of its recent range.

Together, the posts added to the liquidity narrative around Bitcoin. However, the same data also showed a gap between improving money metrics and short term BTC direction.

Global M2 Turns Higher Again as Bitcoin Tracks Liquidity Chart

A chart circulating on X shows global money supply climbing and annual growth turning higher again, as Bitcoin trades near the top of its recent range. The post came from crypto commentator Crypto Rover, who wrote that “Global Liquidity is surging,” while sharing a CoinGlass graphic titled “Bitcoin Price and Global M2 Supply & Growth.”

Bitcoin Price and Global M2 Supply Growth. Source: CoinGlass / X

The chart overlays three series: Bitcoin’s price in gold, global M2 supply in a light blue line, and global M2 year over year growth as vertical bars. The M2 supply line trends upward across the full period and finishes near the upper end of the scale, while the growth bars shift from earlier negative readings to positive territory in the most recent section highlighted on the right side.

Bitcoin’s price line rises alongside prior periods of stronger M2 growth on the chart, then moves through extended swings as the growth rate cools and later recovers. In the latest portion, the gold line sits near the upper band of its recent levels, while the M2 supply line continues to edge higher and the growth bars print larger positive readings than earlier in the year.

Analysts often use global M2 as a broad proxy for liquidity conditions because it reflects the amount of money in circulation across major economies. However, the graphic does not show causation, and Bitcoin can diverge from liquidity measures for long stretches due to market structure, leverage cycles, policy expectations, and crypto specific shocks.

Even so, the shared chart frames a simple message: as global M2 supply expands and the growth rate improves, Bitcoin remains closely watched for whether it follows the same direction seen during prior liquidity upswings.

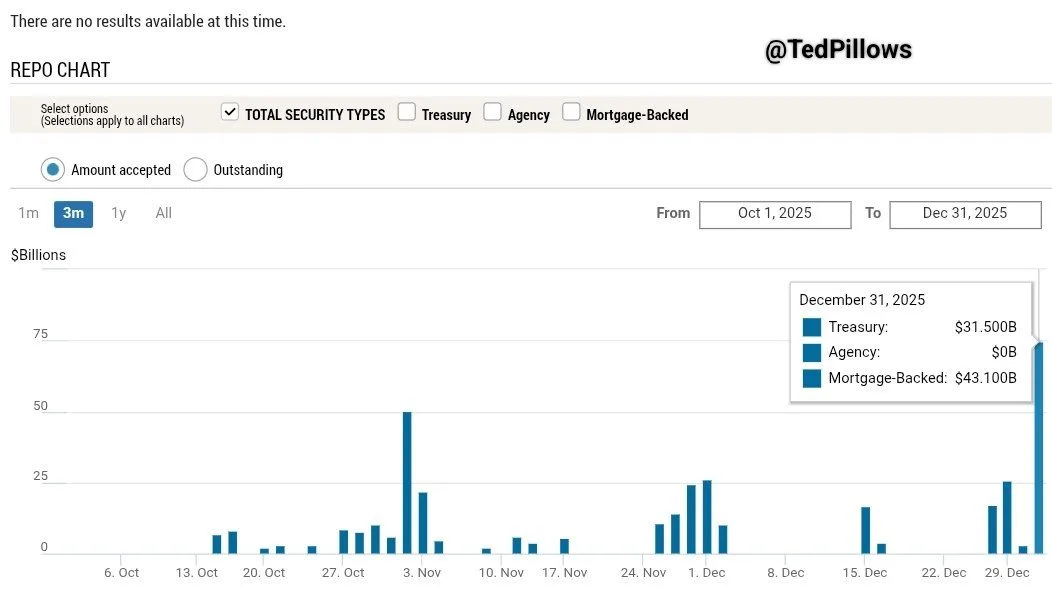

Fed Repo Operations Add Fresh Liquidity as Bitcoin Holds Range

Meanwhile, a chart shared on X by Ted Pillows shows the U.S. Federal Reserve adding sizable liquidity to the financial system through recent repo operations, even as Bitcoin price action remains largely unchanged. According to the chart, the Fed injected about $74.6 billion into the U.S. economy over the past three months, based on accepted repo amounts.

Federal Reserve Repo Liquidity Injections. Source: Federal Reserve via Ted Pillows

The graphic covers the period from Oct. 1 to Dec. 31, 2025, and breaks down liquidity by security type. Treasury repos accounted for roughly $31.5 billion at the end of December, while mortgage backed securities made up about $43.1 billion. Agency securities showed no activity in the latest snapshot. The data reflects short term funding support rather than a shift in long term monetary policy.

Repo operations are typically used to stabilize funding markets and manage short term liquidity needs. As a result, these injections often fluctuate around quarter ends or periods of higher funding stress. The chart highlights several spikes in late October, early November, early December, and again near year end, with the largest bars appearing in the final days of December.

Despite the increase in liquidity shown on the chart, Bitcoin has not posted a clear directional response over the same window. Price action has stayed range bound, suggesting that short term repo injections alone may not be enough to drive immediate moves in BTC. Market participants often distinguish between temporary liquidity operations and sustained balance sheet expansion when assessing potential impacts on risk assets.

The chart reinforces the ongoing debate around how closely Bitcoin tracks liquidity conditions, especially when injections are technical and short lived rather than structural shifts in monetary stance.